(Left: Atlanta Real-time US GDP Estimate / Right: Personal consumption expenditure accounts for approximately 67.9% of Q1 GDP)

The Atlanta Fed's Q2 2026 GDPNow has fallen from over 4% to 1.3%.

GDPNow is a real-time estimate, not a confirmed figure.

Since household consumption accounts for approximately 68% of US GDP, it is important whether consumption can be sustained going forward.

(US Retail Sales, YOY)

Current US consumption is solid.

Retail sales and real consumption are increasing.

However, retail sales are nominal figures that do not remove inflation,

so they include not only actual sales volume increases but also the effect of revenue growth from price increases.

(Left: Personal Savings Rate / Right: Credit Card Delinquency Rate)

The problem is the sustainability of consumption.

The personal savings rate fell to 3.0% in May.

While credit card delinquency rates have decreased, according to reports, some high-interest credit card debt may have been

shifted to relatively lower-interest personal loans.

(https://www.investopedia.com/drowning-in-high-credit-card-rates-americans-turn-to-a-cheaper-lifeline-11947396?)

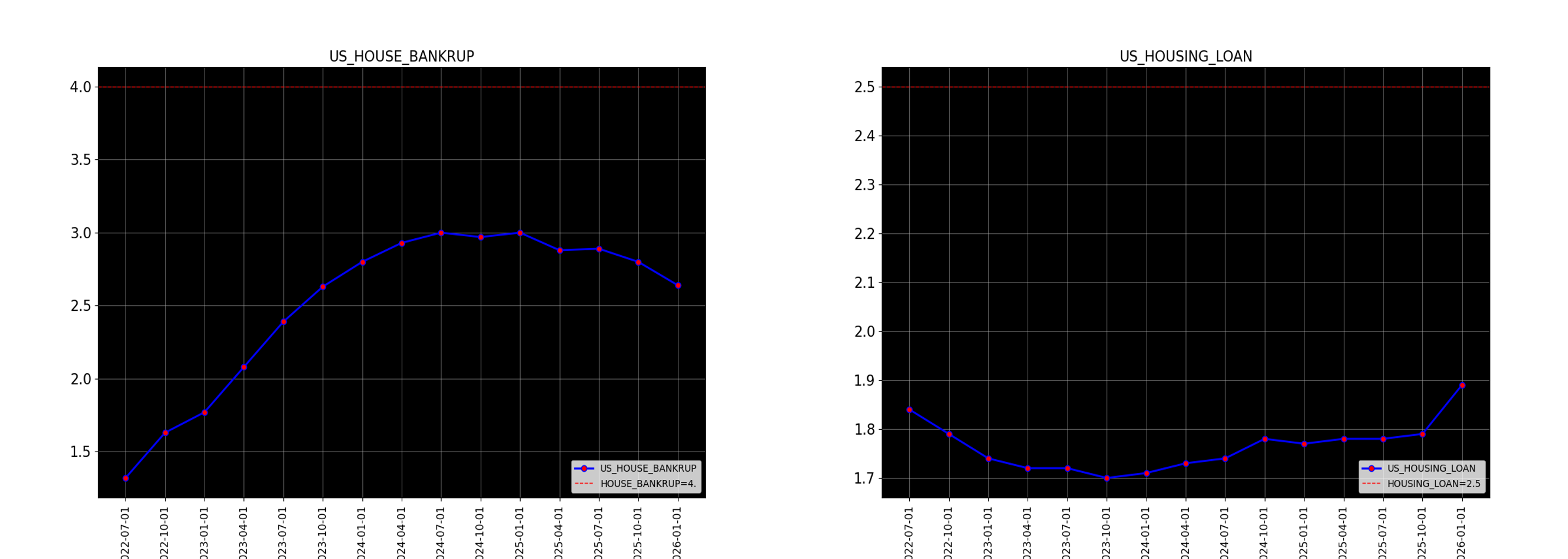

(Left: Household Debt Repayment Burden Ratio / Right: Mortgage Delinquency Rate)

While household debt repayment burden warnings are declining, mortgage delinquency rates have risen slightly.

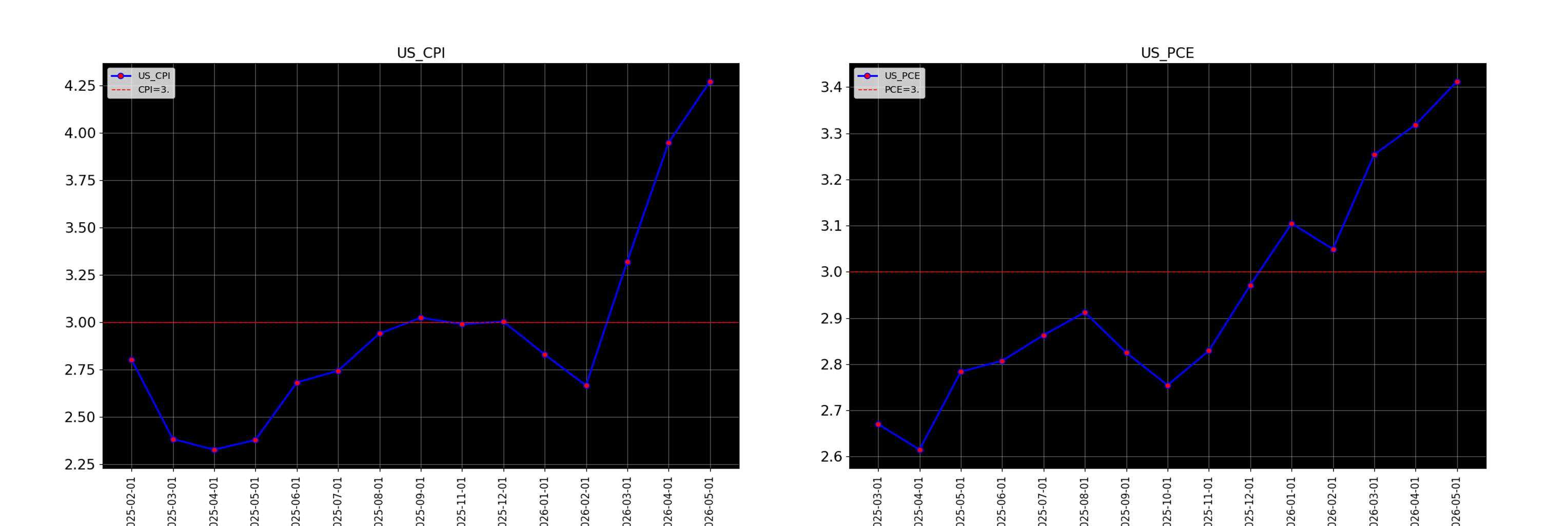

Additionally, the rise in oil prices due to the US-Iran conflict, starting from retail prices,

is now time to impact the prices of all products.

In other words, we cannot rule out the possibility that American households are maintaining consumption by spending cash accumulated over time and shifting high-interest credit loans to relatively lower-interest personal loans.

The recent rise in US 2-year Treasury yields can be seen as a signal that expectations for rapid rate cuts have weakened.

The market appears to be watching for both high inflation and the possibility of prolonged high interest rates rather than economic slowdown.

The current Federal Reserve Chair is Kevin Warsh.

He took office in May 2026 and is traditionally evaluated as having hawkish tendencies that emphasize price stability and monetary policy credibility.

While nominated by President Trump, interest rate decisions are made by the judgment of the entire FOMC, not the President's demands.

My forecast is a hold on rates and hawkish commentary.

Consumption is still strong and inflation is high making cuts difficult, but rapid increases are also difficult due to slower growth rates.

However, depending on various economic indicators released in July, I believe we cannot rule out the possibility of keeping rates on hold while issuing a very strong warning to the market.